This post is sponsored by C Space. Regardless I only post about legitimate offers from trusted sites.

Ever wish you could share an idea directly with a brand to help create positive change? C Space specializes in bringing the customer and the brand closer together, so they can create impactful growth with their combined opinions and ideas.

You’re invited by C Space to join one of their newest, private online communities, where you can be an adviser to all your favorite brands, like Twitter, Unilever, Colgate, or Godiva (to name a few). Interact with others like you, engage in activities, surveys and discussions that interest you, and earn Amazon gift codes for your participation.

I’m currently involved with 2 brand programs like this. I love it. I love being able to tell the company what I like and don’t like and share ideas in an inviting way. And getting the Amazon gift cards for doing that is icing on the cake!

Maybe you’ve just put your Christmas decorations away or maybe you still have them up. (I do, I’m avoiding it) But to create a financially stress free Christmas you need to start saving now. Start saving now to avoid using credit cards, start saving now to avoid overdrafting your account trying to squeeze gifts in, save now so you’re not so stressed later.

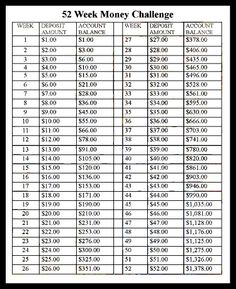

You might have seen the weekly Christmas savings plan that’s floating around on the internet:

Here’s my issue with this challenge. Actually I have several issues. IF you are actually on a budget or living paycheck to paycheck, in theory, this sounds like a great idea. So you start saving $1 in saving the first week, $2 in savings the next week…hey this is easy right? Ok well then you get to about week 30 and you’re putting $30 a week away. If you get paid biweekly, that’s $60 per pay, $120 per month! If you’re living paycheck to paycheck or already putting money in savings for a safety net (as you should) then this is unrealistic. Then you come down to week…i don’t know 46, 47 where you’ve probably started shopping for Christmas with black friday and cyber monday. Who can put $50 a week away when you’re already buying Christmas gifts? I mean if you can, good for you, but you probably have a little more free flow with your money than others.

So I’ll tell you what I do. As a mom of 4 living the frugal lifestyle. As soon as I finish my Christmas shopping whether it be Black Friday or Christmas Eve, I start putting money back into my holiday club to start replenishing for next year. I get paid biweekly so I put anywhere from $5-$20 per paycheck away, EVERY paycheck. Whatever I can afford to take out of that paycheck and still pay bills and have some fun and incidentals money. If you get paid weekly try putting $5-$10 a week away. If you get paid monthly try putting $20-$30 away per pay. Then, Any other non-paycheck money that comes through such as tax returns, winning money on a scratch off, put a percentage of that away too.

If you put $20 a month away until November That’s $220

IF you put $30 a month away until November that’s $330

If you put $40 a month away until November that’s $440

Then if you put other money away for example you get your tax return and you put $100 of it away you can add $100 to your total. Say you won $60 at a football game for their 50/50 you can put $20 of that away. If you get a holiday bonus you could put 20% of that away, etc. You can see where you can build on your savings. Depending how much you spend on Christmas the monthly amount might be enough for you.

Everyone’s financial situation is different, put what you can away. You can actually use this idea for your safety net savings as well.

One thing that always seems to be a big financial stresser is medical bills. You don’t choose when and where you get hurt or sick and you can’t very well ignore chest pains or a broken bone. Even with insurance medical bills can be overwhelming. If you find yourself with mounting medical debt or are expecting a big medical bill (labor and delivery for instance) here are some suggestions to prepare yourself for the future or help you if you’re already buried in medical debt.

Planning ahead:

–If your employer offers health insurance and you can afford it, do it. If you can get a secondary insurance under your spouse without too much money, this can be a good idea too. Then when one insurance won’t pay, it’s possible the secondary could pick it up if it’s a covered expense.

–Flexible healthcare spending accounts. This can be a way to manage debts you anticipate such as regular doctors appointments, prescriptions, or ongoing medical supply needs such as glucose test strips, etc. Some employees and even banks offer flexible healthcare spending accounts. You can specify an amount per paycheck to be taken out and put in the account. $5 per pay, $20 per pay, whatever you like. Then when you pay a medical bill, buy medial supplies, or fill prescriptions you turn your receipts in to get the cash from your flexible spending account. The downfall is, even though, it’s your money, you must use what’s in the account every year or you lose it. So you probably don’t want to overestimate how much you put in there.

–Supplemental insurance policies. There are more and more supplemental insurance companies out there. They are not health insurance but it’s a policy you pay into to help cover expenses later in the event of a medical issue. Companies like AFLAC and Lincoln, for example, offer policies that will pay you cash payments depending on your situation. They can also help pay for expenses insurance doesn’t cover, hotel stays, travel to specialty treatments centers, etc.

–Savings accounts, this can be said for anything in life, not just medical expenses. All the financial experts recommend having enough money in your savings account to cover in the event of loss of job or hardship. Depending on which one you follow, they recommend anywhere from 6 months to 1 year worth of salary in savings. I know this seems a bit impossible for those of us that are living paycheck to paycheck. Consider opening a savings though and depositing even $5 a paycheck and leave it in there. Let interest work for you to give you some free money. You never know when you might needs some money for unexpected medical bills, car repairs, etc.

–If you’re employer doesn’t offer insurance or you can’t afford it you can see if you qualify for free or low cost health insurance at healthcare.gov. Some states also have programs for children. One example would the the CHIP program in Pennsylvania.

picture credit to pixabay.com

Dealing if you’re already under medical debt:

–First make sure all the charges are valid. It’s easy, when you’re getting bill after bill, to think you actually do owe it. Just from personal experience, we had a bill that my husband paid. Thankfully he wrote down the account number and kept the stub. They kept sending us bills threatening to send up to collections. He called several times and had to raise a little heck but after several people looking at it. It was a mistake in their computer billing system and we had, in fact, paid it.

–See if the medical facility you’re receiving the bill from has a payment plan. Some may even offer financial assistance or hardship programs if you qualify.

–If you’re already under collections make payments the best you can, even if you only send $5 per bill. You’ll be making an effort to pay. Yes they can still send you to collections even with making small payments.

–See if the debt collectors will settle. Debt collectors are hired by the companies you are in debt to. They want to collect the money. Sometimes debt collectors will settle a debt for a fraction for the original full amount. Do be honest with them. Tell them your situation and what you think you can actually pay. If it’s $10/month tell them that. Debt collectors are not allowed to harass, threaten you, or use obscenities when talking to you. For consumer information on what debt collectors can and can’t do you can check out the FTC government site on debt collection.

–Borrowing money from whole life insurance policies – This only works for whole life insurance policies and not term life insurance policies. Depending on how long you’ve had your whole life policy, how much it’s for, and the terms of your provider you can borrow money from your whole life insurance policy. This is a better option than taking out a loan or using a cash advance.

Last Resorts

Ok so maybe you tried all this stuff and you’re in a spot that none of this can fix. There are options. I do NOT recommend these unless you have no other choices

–Bankruptcy , I know that’s a dirty word. But for someone who is in way over their heads with no relief in site, this can at least relieve some stress. Chapter 7 wipes out all qualifying debt but if you own a home or cars that you’re behind on you could risk losing those. Chapter 13 combines all your debt and gives you a settlement payment you must pay each month. It’s a fraction of what the normal debt monthly payments would be. This one allows you to keep your house and cars but you will have to make monthly payments. It’s kind of a reset on your payments.

—Selling life insurance policies, again I don’t recommend this unless you absolutely have to. Yes you can sell life insurance policies,the link at the beginning of this listing give you information. You can get money to help pay debts but it also means your loved ones will no longer receive any benefits upon death.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

{kind=link}